The most entertaining and dramatic stock to follow these days of course is Tesla. Its sky high market cap has drawn fanatic proponents as well as adamant critics into the public discourse. One of the main arguments made by bulls is the idea that Tesla should not be valued as a car manufacturer, but rather as a Tech company. They say the coordinated software development, innovative design, and Silicon Valley location all warrant this notion. These points are all true, but are of course only ancillary to Tesla’s core business—car manufacturing. Although, many hopeful Tesla investors are expecting the parabolic returns that household tech giants have achieved in recent years.

Here we will give Tesla bulls the benefit of the doubt in our analysis. We will assume that Tesla is destined to be a true tech giant, justifying the troubling net losses with the promise of rapid growth in the future. We set aside the differences in business models and capital structure in an attempt to create a basic comparison of early stage tech companies. We took a sample of 4 major tech companies, Apple, Twitter, Facebook and Amazon, and rewound the clock to the earliest comparable financial period. Twitter, although maybe not fitting into the “big tech” category, was tracked as well to show in stark contrast to its more successful peers. As you will see, Twitter’s poor financial ratios were an indicator of a declining stock for years to come.

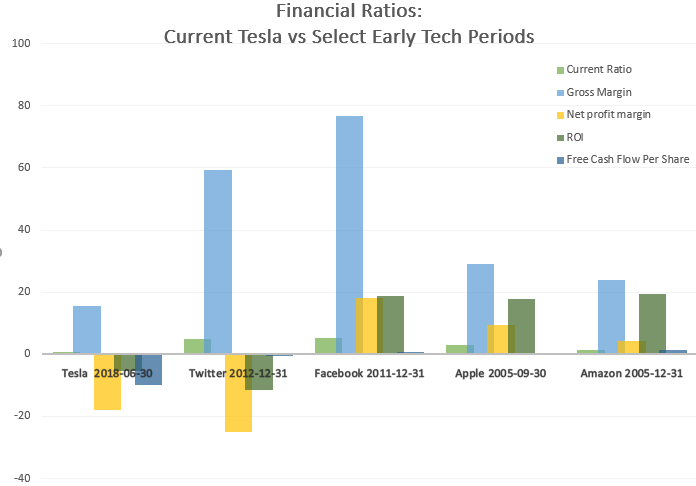

The Numbers

For the analysis, we narrowed in on periods where each company was in a similar stage of development as Tesla right now(focused on scaling and having little to no earnings). We gave Tesla’s valuations the best chance possible at outperforming by selecting the earliest and most weak reporting periods we could find as benchmarks for Tesla to beat. One caveat is if there was an extreme outlier in the data from period to period, the next period was used instead. We avoided data that was skewed by one-off events. In a nutshell, we tried to compare the Tech giants at their worst vs Tesla at it’s best. All else being equal, positive values are what is desired in these 5 metrics.

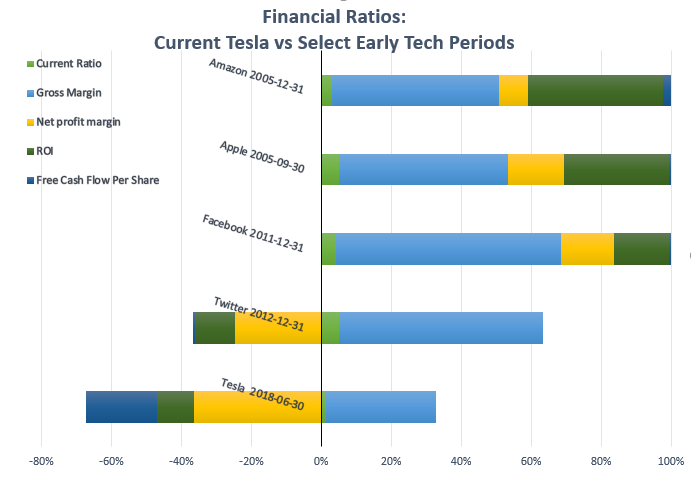

As you can see, Tesla’s financial ratios are the worst performing in almost every one of the 5 companies compared. The current ratio is low, showing how Tesla is strapped for cash to cover its short term liabilities. This is probably why Tesla took drastic measures to get better A/P terms from suppliers earlier this year. Gross margin is the only redeemable metric that shows something positive. Tesla has no doubt strained to keep it so, moving certain expenses such as warranty expense, normally included in COGS, further down on the income statement. Accordingly due to the top-line flexing, their bottom-line numbers have been sacrificed. Tesla has a terrible Net Profit margin. ROI and FCF are similar stories. Below is that same chart viewed as a 100% bar to further illustrate how far behind Tesla is from its would-be peers:

When judging from these metrics we can see that TSLA has a lot more in common with early Twitter than early Facebook, Apple, or Amazon. Though in most cases it’s even worse than Twitter.

“Selling a dollar for 75 cents.”

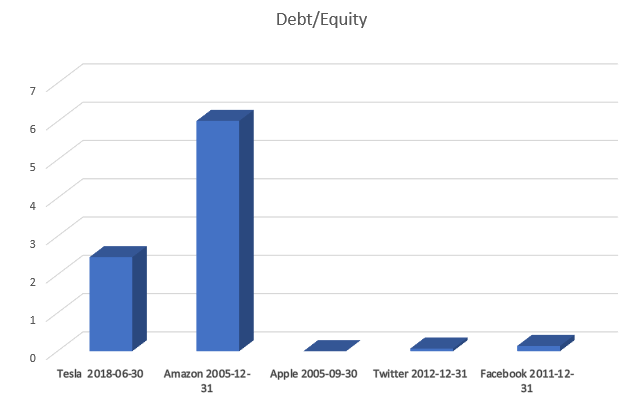

Tesla only fares better in debt/equity ratio when compared to Amazon, a profitable business at the time.

Note one parallel, Amazon some years after its IPO was in rapid scaling mode. Profit targets repeatedly missed analyst expectations, but on revenue it beat expectations. Tesla has had similar quarters recently. Proponents will point out this one similarity with Amazon as a normal part of a scaling business. However, Amazon was profitable at the time, whereas Tesla is currently not even close. Revenue beats and earnings misses are ok when you’re already showing some profits. For Tesla on the other hand, revenue beats when earnings are getting worse is an entirely different story. Accordingly, Amazon could warrant the high amount of debt on it’s balance sheet.

If early Twitter’s close financial metric similarity to Tesla(besides its debt levels) is any indicator as to the direction of the stock, we might expect some wild volatility, before finally crashing to about half it’s current value over the course of a few years…Short sellers might feel quite a bit more pain before it resolves itself. Does Tesla make cool cars? Yes. Will Tesla still be around in the future? Of course. Is the stock overvalued? We think so!

Leave a Reply